OFFICE rents in Singapore’s central region fell 0.5 per cent in the third quarter of 2024 over the preceding quarter, contrasting with the 3.1 per cent quarter-on-quarter (qoq) increase in Q2 2024.

The increase in the first nine months of the year amounted to about 0.8 per cent, a much slower pace of growth than the 12.8 per cent expansion in 9M 2023, said Leonard Tay, head of research at Knight Frank Singapore.

“During the quarter and throughout most of the year, relocations and expansions from larger office occupiers, both domestically and cross-border, were few and far between. This is on the back of (capital expenditure) constraints due to global economic uncertainty,” he said.

Analysts also pointed to other signs of weakness in the Urban Redevelopment Authority’s (URA) latest office market data, released on Friday (Oct 25).

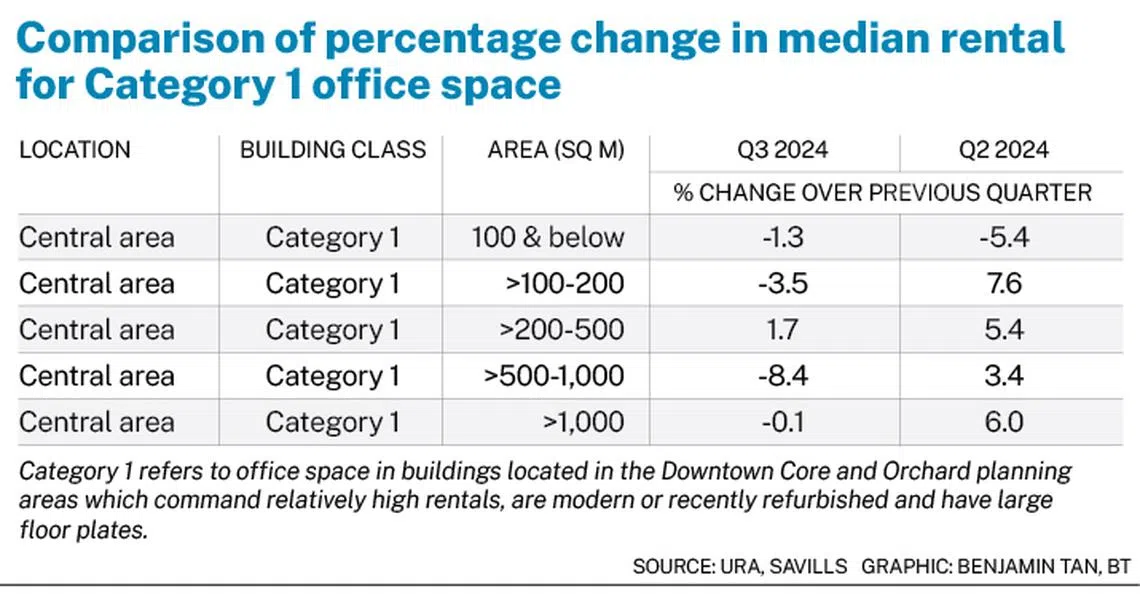

Tricia Song, CBRE’s head of research for Singapore and South-east Asia, highlighted that URA’s median monthly rental (based on contract dates) for Category 1 offices – which cover the better-quality buildings in the city area – shed 0.8 per cent qoq in Q3 2024 after a significant 4 per cent increase in Q2 2024.

“CBRE Research attributes this softness to a recent surge in supply, notably the completion of IOI Central Boulevard Towers, which added 1.2 million square feet of prime office space in the (Central Business District),” she said.

A NEWSLETTER FOR YOU

Tuesday, 12 pm

Property Insights

Get an exclusive analysis of real estate and property news in Singapore and beyond.

Consequently, vacancies in Category 1 office buildings rose to 10.3 per cent in Q3 2024, from 7.5 per cent at the end of 2023, she added.

The roll-out of AI solutions…will supplant the return-to-office call by employers.

ALAN CHEONG OF SAVILLS

”

Delving deeper into URA’s Category 1 rents, Savills Singapore executive director Alan Cheong pointed to signs of “a rapid turnaround for rents for this category of office space in the third quarter”.

“Although there is a possibility of qoq rental volatility involved, feedback from the ground – that tenants are gunning for right-sizing, and tech companies, too, are downsizing – is building a case that the decline may not purely be due to short-term fluctuations,” he said.

Islandwide, the amount of occupied office space increased by 17,000 square metres (sq m) of net lettable area (NLA) in Q3 2024, against the decrease of 20,000 sq m in the previous quarter. However, the stock of office space continued to increase, to the tune of 36,000 sq m of NLA in Q3 2024, after expanding by 87,000 sq m in Q2 of this year.

The islandwide office vacancy rate rose to 11 per cent as at end-Q3 2024, from 10.8 per cent as at end-Q2 2024.

Cheong expects a sea change in the way tenants behave in their workspace requirements as they begin adopting artificial intelligence (AI) in their workflow.

“From 2025 onwards, we believe that the roll-out of AI solutions by Big Tech companies to end users will mean a sweeping change in the number of employees required in a new worker-AI partnership relationship.”

He added: “This will supplant the return-to-office call by employers, and possibly lead to even fewer workers needed in an office.”

CBRE’s Song, too, noted that with market conditions expected to be soft “at least in the near-term future”, some projects in the city area – such as Keppel South Central in Hoe Chiang Road and the Shaw Tower redevelopment in Beach Road – have yet to register pre-commitments.

“While this could weigh… on rent expectations, there has been some relief in terms of supply injection”, including the completion of Shaw Tower’s redevelopment being delayed to 2026, and the URA’s decision not to award the Jurong Lake District master developer site,” she added.

Also sounding a positive note was Cushman & Wakefield’s research head for Singapore and South-east Asia, Wong Xian Yang, who said office leasing activity may pick up towards 2025, fuelled by interest from emerging tech industries, wealth management firms and professional services companies.

He added: “Demand for offices in the central region is expected to be supported by a tight labour market and high office attendance, driven by strong return-to-office mandates.”

URA’s data also showed that prices of office space in the central region rose by 0.6 per cent in Q3 2024, moderating from the 3.1 per cent gain in the previous quarter. Nevertheless, Tay of Knight Frank sees interest rate cuts stimulating more sales of strata offices and office buildings.

Retail market data

URA’s latest data also showed that rentals of retail space in the central region rose 0.3 per cent qoq in Q3 2024, after remaining unchanged in Q2 2024. The islandwide vacancy rate of retail space dipped to 6.5 per cent as at end-Q3 2024, from 6.6 per cent as at end-Q2 2024.

Prices of retail space rose 1.7 per cent in Q3, in contrast with the 1.2 per cent drop in the previous quarter.