What is negative interest rates and what are the effects of negative interest rates on the economy? To get started, check up this news on how a Danish bank is paying borrowers to loan out their money. Doesn’t make sense? That’s what the world is heading towards now. Let’s take a look at the interest rate trends in 2019. This would probably be a good summary for the uninitiated.

1. Fed Cutting Rates

The fed has cut interest rates 3 times in 2019. From the last financial crisis in 2009, we have lived in a period of ultra-low interest rate environment where the money supply is cheap and easily accessible. Debt piles up and business expands on cheap liquidity. The stock market rallies and investors rejoice.

Interest rates started rising in 2016 to 2019 before plateauing at 2.5%. The reason why rates are increased is usually to slow inflation and cool down an overheated economy. But why stop in 2019? Perhaps companies and government have borrowed too much money. A further increase in interest rates would be too much of a financial burden to bear.

Now, this poses a potential problem. From a grand scheme of thing, you can see that interest rates used to be much higher in the past. When the economy is up, raise the rates, when the economy is down, lower the rates. Rates have traditionally been used as a monetary tool to control the economy.

But now the world is struggling at 2.5% interest rate. What happens if interest rates are not able to be raised. We would start moving lower and lower to 1%, 0% then what’s next? What monetary tools do we have to stimulate the economy at 0%? This is what happened to Europe and Japan.

Hooray! Interest Rate Cuts…

Since July 2019 to Oct 2019, the fed has cut fed rates by 25 basis points each time and now we are at 1.5% – 1.75%. During this period of time, the stock market rallied hard and the index makes higher highs. You would often see headline news titled: “Dow tops 28,000 or S&P 500 close at record high”.

Trump is happy because elections are up around the corner in 2020. Investors also became rich as asset prices went up and up as if there is no end to it. But what is interesting is a recession typically ensures right after 3-4 rounds of interest rates cut. Maybe this time is different?

Most people view rate cuts from a very simplistic and logical point of view. When the fed cut rates, interest expenses go down, businesses & individuals borrow more, spending increases and profitability margins go up. Economic growth is stimulated, GDP goes up and a rising tide lifts all boats.

However, what people don’t think about is the underlying reason why fed cut rates? While news media outlets boast about low unemployment rates and a strong economy in the US, then why the rate cuts? Rate cuts are meant to kick start and stimulate a weak economy. It is obvious that cracks are showing up in the system and they know something that we don’t.

And to what extent does low interest rate stimulate the economy and increase productivity? What if all the new supply of money is just stored in the reserves of banks, refinance previous debts, used for investments and do stock buybacks, then there really isn’t any economic output. If the debt rises much faster than GDP, income would start to fall short of payments and we are just living on borrowed time.

2. Negative Interest Rates in Europe & Japan

The negative rate phenomenal is unprecedented in monetary history. But it seems that it has become the norm as certain countries such as Switzerland, Denmark, Sweden and Japan have allowed rates to fall to slightly below zero.

How it works is that Commercial banks usually have to deposit a certain % of cash reserve with central banks. Do check up the previous post on “Minimum Cash Balance” to understand the reasons behind.

When central banks charge negative interest rates, it punishes banks for parking their money there. The purpose of negative interest rates is to encourage banks to loan out money supply to borrowers and stimulate the economy.

On the other side of the coin, savers have to pay for depositing their money in bank accounts. Instead of receiving say a 2% annual interest on your deposits, you have to pay 0.5% to the bank for storing money in the bank.

Banks, of course, won’t do this as depositors would shun away and store cash under their mattress. This directly affects the quantum of money they can loan out under fractional reserve lending. If negative rates sink deeper, it is likely that the bank would absorb the cost and see net interest margin compress further.

Why Negative Interest Rates?

Negative rate is a last-resort measure to force people to spend rather than let their cash idle. This is because the Japanese are big on saving and hoarding cash. It is the first of a kind and it is implemented because the ultra-low interest rate is unable to stimulate the sluggish economy and low inflation.

This brings up an interesting point. Do things really go according to the macroeconomic theories or is there a big disconnect? Europe started experimenting with negative rates in 2014 and Japan in 2016.

If the low-interest rate is able to spur consumer spending and boost inflation, then why did it fail and why are rates becoming negative now? GDP stays low and inflation remains flattish in Europe and Japan. Something is obviously not working.

We are in uncharted territories and the degree of magnitude in how this would play out is unknown yet. This is especially the case for negative rates. It has not been taught before in the textbooks of modern finance since this is the first time we see such a phenomenon.

3. Repo Market Problems – QE4 Commenced?

Repo is a banking term which describes the scenario where banks with excess money would lend banks who need liquidity overnight using collateral such as government treasuries. Tons of cash and collateral are swapped every day. You can read about it to understand better from the previous post on repos.

Usually, repo rates are within the band of the fed fund rates which was 2% to 2.25% back then. But in September 2019, there is a huge spike in the repo market up to almost 10%. This means that there are banks who are willing to pay 10% interest to borrow money as they have insufficient cash and liquidity.

There is a shortage of money supply in the banking system which caused repo rates (rates which banks lend to each other) to rise up significantly.

How does the Fed solve the repo problem?

In order to alleviate the situation, the fed has to intervene by buying up treasuries to pump money into the system.

The official term is called Treasury Bill Purchases and Repurchase Operations. But it simply means printing money and shoving it into the balance sheet of banks to make it look like it appears healthy. The fed has a plan to pump in $60 billion every month into the financial system until Q2 2020.

No one really knows what happen but the process is reminiscent of QE1, QE2 and QE3 during and after the 08-09 financial crisis. Interestingly, Fed Chairman Powell said this intervention is not a restart of QE. Though from Sep to Nov, we have already seen an approximate of US$300 billion being pumped in.

This can be seen by looking at the balance sheet of the fed in the diagram above. It has increased from 3.75 trillion to around 4.05 trillion since Sep 19. Whenever the fed’s balance sheet increases, it means they have printed money and injected it into the system by buying up treasuries.

4. Implications of Negative Interest Rates

Central banks around the world have followed suit the direction of the fed to lower down interest rates. Here are some of the potential implications or scenarios that have already occurred or might occur in the near future.

(a) Inflating Asset Prices

When money becomes cheap at relatively zero cost, everyone would borrow now and start buying properties, cars and etc. This is especially the case for Denmark where banks pay consumers to loan out their money. A housing bubble might cause a sharp increase in price and rental, which benefits landlords and investors while putting a financial strain on tenants and consumers.

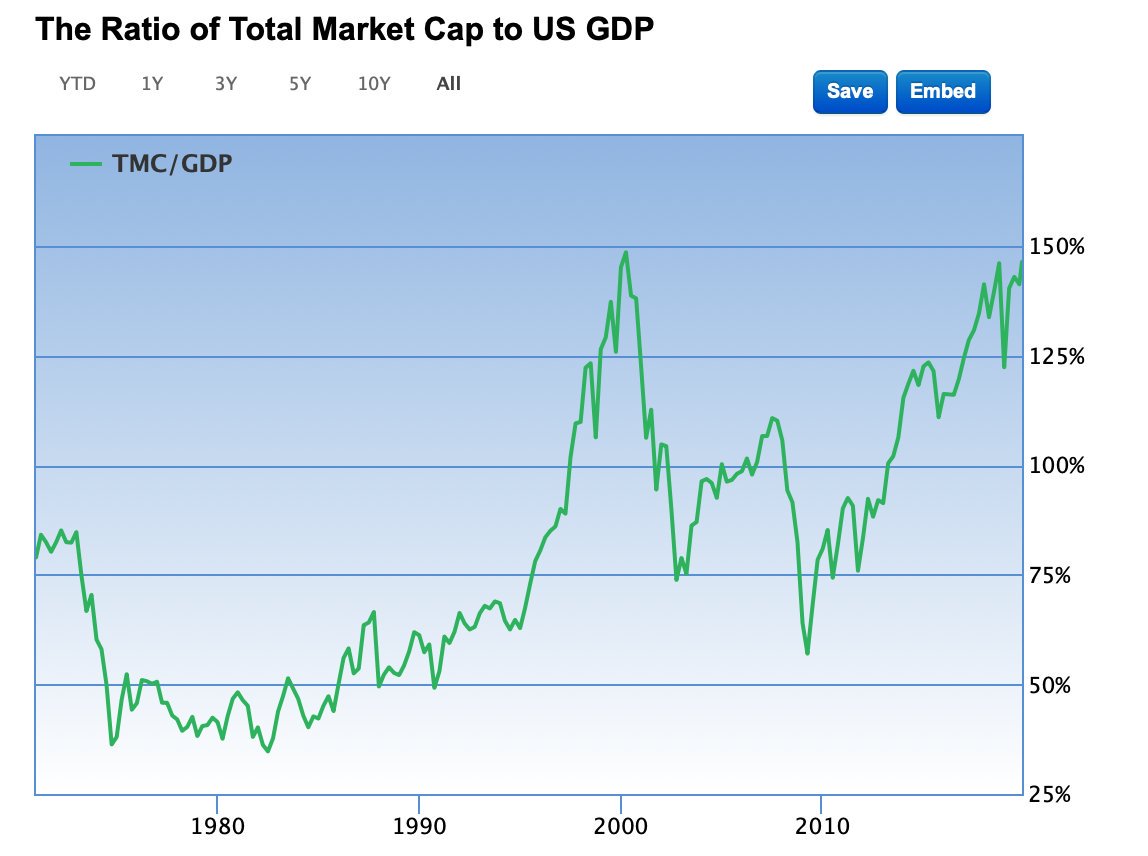

On the other hand, companies can borrow at no cost to do a share buyback so as to jack up stock prices and earnings per share. Even though profits might remain unchanged, earnings per share would still increase since outstanding shares have decreased. This is already happening now as we can see that it is debt that pushes the stock market prices up rather than fundamentals. Take a look at the ratio of total market cap to GDP.

Lastly, proponents of discounted cash flow analysis would also start seeing the valuation of assets rise significantly as the discount rate falls. But if it falls to negative, I really don’t know if doing a DCF even make sense. A negative discount rate is essentially saying the expected return of an investor is a loss.

(b) Currency Devaluation

Since the US dollar is the reserve currency, whenever the fed cut rates, other countries are likely to follow suit. When the fed cut rates, investment returns in the US falls which causes money to be withdrawn thereby devaluing the currency.

A weaker US dollar boosts exports and increases market competitiveness as its currency became cheaper relative to other nations. Export-oriented countries would be disadvantaged as a weaker US dollar means a lesser purchase of goods and services.

To maintain their competitive advantage, most central banks in other countries would also lower rates if the fed cut rates. This might lead to a competitive devaluation of fiat currencies on a global scale.

Trump is a big advocate for zero and negative rates. He has called the fed “boneheads” and often criticised the fed for cutting rates too slow. Perhaps this is to reduce US trade imbalance and make the stock market rally even higher. Imagine what would happen to the world when the US goes to a negative interest rate.

(c) Trouble in Insurers and Pension Funds

Insurance companies and government pension funds face a huge risk if the return on investment continues to fall. They have a financial obligation to payout retirees a certain % of returns monthly/quarterly/yearly. All these promises or liabilities are made long ago when some sort of contractual agreement has been signed.

Insurance companies and pension funds typically profit from the spread they made by using your money to invest in other assets that yield higher returns.

The fed rate is usually used as a baseline for the risk-free rate. If it falls, the yield of other asset class such as bonds and equities would likely fall. The trouble comes now when all the yields are being compressed below the rate at which they have to pay out their obligations.

Let’s say I promise to pay you 5% but the investment return out there is only 1%. Where do I fork out the loss of 4%? Announcing a cut on the payouts to pensioners would stir huge social unrest. It would probably be the last resort as that would be a political suicide move.

Pension funds would begin to move towards riskier asset to chase for higher returns that compensate for their liabilities. But they also have regulatory limitations on the level of risk they can take. The easy way out? Print more money.

(d) Widening Wealth Inequality

When the rates are lowered and money is pumped into the system, where does it go? One thing for sure is that it doesn’t go into the pockets of yours and mine. But it depends, on whether you own assets.

If you own properties, stocks and etc, the money would pump up the value of your assets. Just compare the net worth of someone who bought the S&P 500 and someone who didn’t.

As mentioned earlier in (a), debt is used to buy back shares and increase share prices and the stock market. If you own a piece of it, you get to ride the rising tide. But what % of the population owns stocks? The rich get richer and the savers become poorer due to inflation.

And also, the more accurate way of looking at this is not the value of your property has went up, but rather the value of your dollar has come down. As the money supply increases, the value of the currency depreciates.

(e) Declining Profitability of Bank Margins

This is just a theoretical possibility. Till date, there is no conclusive evidence that suggests negative interest rates would hurt bank margins. Because we are so new to this. When interest rates fall, banks would start collecting lower interest income from borrowers.

But this would be offset by lower deposit costs and the increased volume in lending activities. In times of low-interest rate, people borrow more to buy a house, buy a car and businesses borrow more to refinance previous debts or expand their operations. All works fine so far.

But the problem comes when rates hit zero or turn negative. Banks would be reluctant to charge negative rates or they would see a flight of capital from all the small depositors. An interest floor limit is being placed on depositor’s savings or fixed deposit accounts.

Net interest margins would start compressing if what they pay depositors remain fixed but the interest rate they loan out to borrowers start decreasing. This would force banks to take on even riskier loans similar to the case of pension funds.

(f) The bull case for bitcoin and gold

In times like this, the winner that emerges is usually gold or bitcoin. In the previous post, it was mentioned that none of the fiat currencies survived for the past 5,000 years. All of them eventually went to zero due to excessive printing of currencies. What makes the US dollar or the Yuan different?

The case of a recession may or may not come, even though it is already due. You never know what the fed and central banks can do to distort the natural forces of markets. They can continue to print money, ease monetary policy and this can go on and on to artificially boost growth through zero-cost debts. The market can stay irrational longer than you can stay solvent.

This is simply not sustainable and the house of cards would eventually collapse. During the next recession, gold and maybe bitcoin would see their value rise significantly as investors rush back to these safe-haven assets. Of course this is all speculative.

This is especially the case for bitcoin. The 2020 recession theme and bitcoin halving in 2020 is perfect coincidental timing. The crypto market has never before coincided with a recession in the traditional financial markets. After all, bitcoin was created in 2009 during the last financial crisis as an alternative solution. It would be interesting to see how all this plays out for crypto during the next recession.

All it takes is just a blip or a black-swan event to start the domino. It could be the bailout of banks in China, the derivatives from Deutsche bank, pension rate cuts, breakdown in US-China trade deal, bank troubles or anything. When the last straw broke the camel’s back, all hell will break loose, as it should in a natural cycle.

The post The Effects of Negative Interest Rates appeared first on The Babylonians.